How Accrual Automation Improves Technology Expense Management

May 31, 2026

Cost Control

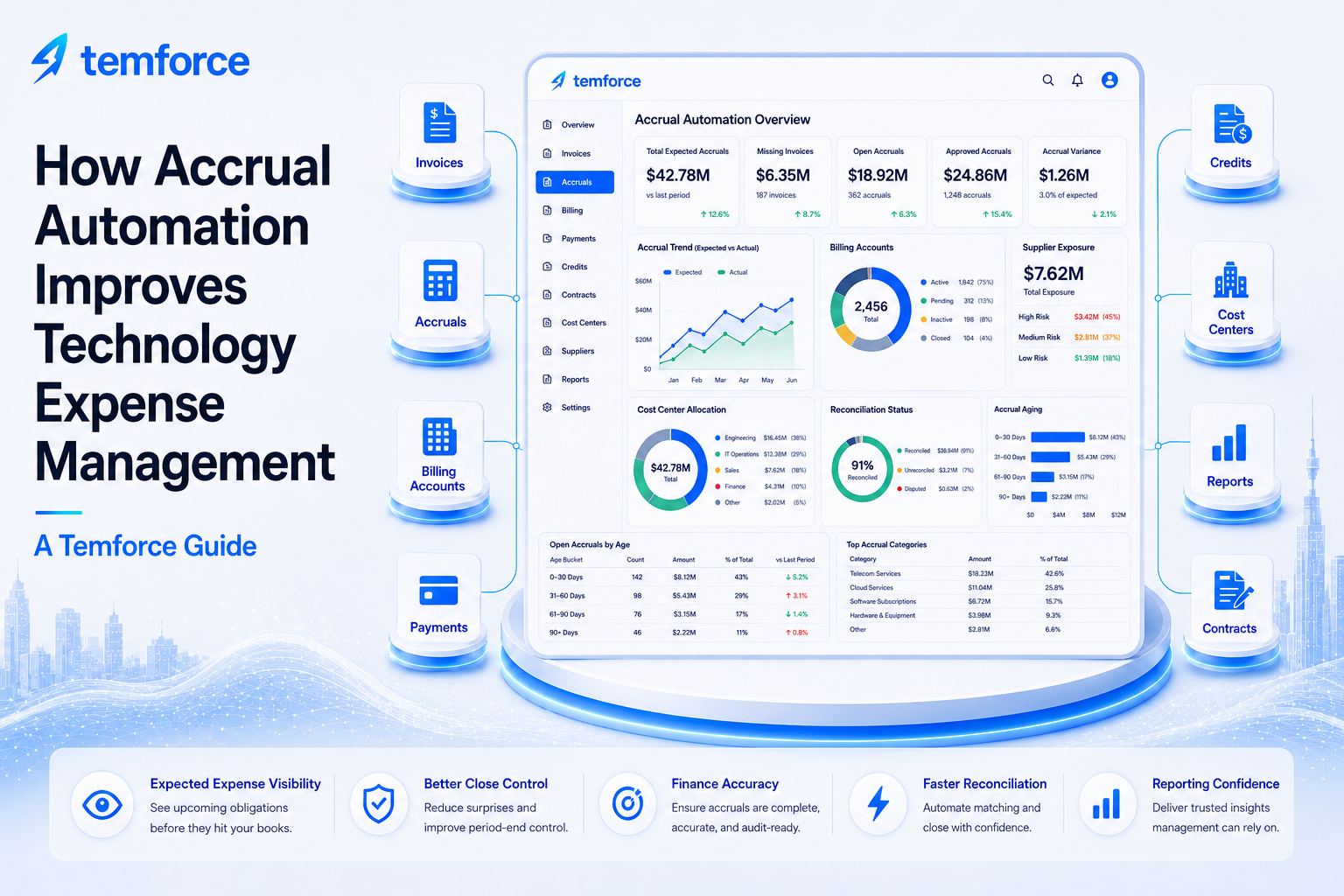

Accrual automation improves technology expense management by helping finance and TEM teams estimate expected charges when invoices are missing, delayed, incomplete, disputed, or not yet ready for payment. It connects operational TEM data to finance close so monthly expense reporting is more accurate and easier to explain.

Accruals are where TEM data becomes finance-ready. If an invoice has not arrived, finance still needs a defensible estimate of expected expense. Accrual automation helps turn billing history, active inventory, supplier patterns, contract commitments, and open exceptions into a structured close process.

An accrual should not be a guess. It should be connected to expected invoice activity, active services, billing account history, supplier behavior, contract commitments, cost center ownership, and documented assumptions.

Why accrual automation matters in TEM

Technology invoices do not always arrive in time for finance close. Supplier billing cycles shift, invoices are delayed, charges are disputed, services are added mid-period, and billing account activity may not align perfectly with the accounting calendar.

Accrual automation gives teams a repeatable way to identify expected expense, support finance close, and explain why a number was accrued.

Accrual automation connects missing invoices, active billing accounts, prior charges, inventory, supplier patterns, and expected spend.

Every accrual needs an owner, source data, assumption, cost center, finance treatment, review status, and reversal plan.

Controls help finance capture expected charges even when supplier invoices are missing, delayed, or not yet approved.

Teams spend less time building accrual estimates from spreadsheets, emails, supplier portals, and prior invoices.

Accrual automation helps organizations move from manual finance estimates to governed TEMOps close support. It creates a better bridge between operational activity and financial reporting.

The accrual automation model

A strong accrual model connects missing invoice detection, billing account history, active inventory, expected charges, cost centers, and finance close status.

| Accrual Area | What to Track | Why It Matters | Risk If Missing |

|---|---|---|---|

| Missing invoice signal | Expected invoices, missing invoices, supplier, billing account, last invoice, billing cycle, and period. | Shows where finance may need an accrual. | Expense may be understated if missing invoices are not identified. |

| Estimate basis | Prior-period average, contract rate, recurring charges, active inventory, usage trend, and supplier history. | Creates a defensible reason for the accrual amount. | Accruals may become unsupported manual estimates. |

| Ownership and coding | Finance owner, TEM owner, cost center, GL code, business unit, department, and allocation rule. | Accruals must post to the right financial owner and reporting category. | Expense may be booked to the wrong budget or cost center. |

| Exception context | Disputes, credits, payment holds, supplier delays, corrections, outages, and unresolved invoice issues. | Open exceptions can affect the accrual amount and timing. | Finance may accrue too much or too little without operational context. |

| Close status | Accrual status, approval status, posting date, reversal date, invoice received date, and reconciliation status. | Accruals need a lifecycle from estimate to reversal and reconciliation. | Accruals may remain stale or fail to reverse when invoices arrive. |

| Reporting outcome | Total accrual exposure, variance, supplier category, aging, confidence level, and executive summary. | Reporting helps leadership understand expected expense and close risk. | Accrual exposure may not be visible until after close. |

How to manage accrual automation in a TEMOps operating model

Accrual automation should be part of the recurring finance close cadence. The goal is to identify expected charges, document assumptions, assign ownership, post the accrual, and reconcile it when invoices arrive.

Identify missing invoice exposure

Compare expected supplier invoices and active billing accounts against current-period invoice activity.

Build the accrual estimate

Use prior invoices, recurring charges, inventory records, contracts, usage trends, and supplier history to calculate expected expense.

Assign finance coding

Connect the accrual to the correct cost center, GL code, business unit, department, allocation rule, and finance owner.

Review exceptions and assumptions

Adjust for disputes, credits, holdbacks, supplier delays, service changes, renewals, and known corrections.

Post and monitor the accrual

Track accrual status, approval, posting date, reversal timing, invoice receipt, and reconciliation status.

Report close outcomes

Show accrued amount, open exposure, reversed accruals, received invoices, variance, aging, and unresolved close blockers.

What accrual automation records should track

Accrual records should capture enough detail to support finance posting, audit readiness, variance review, and invoice reconciliation.

- Supplier, billing account, expected invoice, missing invoice flag, billing period, last invoice date, and last invoice amount

- Accrual amount, calculation basis, prior-period average, expected recurring charges, usage estimate, and confidence level

- Active inventory, service count, contract reference, rate plan, renewal impact, and known service changes

- Cost center, GL code, business unit, department, allocation rule, finance owner, and TEM owner

- Dispute status, credit expectation, payment hold, supplier delay reason, and exception note

- Approval status, posting status, posting date, reversal date, invoice received date, and reconciliation status

- Variance amount, variance reason, unresolved exposure, close blocker, next action, and task owner

- Reporting period, dashboard category, executive summary note, and audit evidence

If an accrual cannot be traced to a billing account, expected invoice, inventory record, contract term, supplier pattern, or documented assumption, it should be reviewed before close.

Common accrual automation issues

Accrual issues usually appear when invoice intake, billing account tracking, inventory, supplier status, and finance close are disconnected.

Finance may not know an expected invoice is missing until close reporting is already incomplete.

Manual estimates can be difficult to explain if they are not tied to source records and assumptions.

Missing cost centers, stale GL codes, and unclear owners can create finance reporting issues.

Accruals can remain open or duplicate actual expense if reversal and reconciliation are not tracked.

Delayed invoices need supplier context so finance understands whether the exposure is temporary or recurring.

Leadership may not see how much expense is estimated, unresolved, reversed, or awaiting invoices.

Example scenario: a missing supplier invoice during close

A supplier normally bills $82,000 each month, but the invoice has not arrived before close. Inventory still shows active services and the billing account has a consistent invoice history. In a weak process, finance may scramble for a manual estimate. In a stronger TEMOps process, the missing invoice is flagged, an accrual estimate is generated from history and inventory, the cost center impact is assigned, and the accrual is reconciled when the invoice arrives.

Instead of asking, “What should we estimate?” the business asks, “What source records support the accrual, who owns it, when will it reverse, and how will we reconcile it?”

How Temforce helps with accrual automation

Temforce helps organizations connect accrual automation to invoice intake, billing accounts, inventory, suppliers, contracts, cost centers, GL codes, payment status, reports, and dashboards.

The goal is to move accrual support away from manual close spreadsheets and toward a governed TEMOps process with clear source data, assumptions, finance ownership, approval status, reversal tracking, and reporting confidence.

Identify expected supplier invoices, missing billing account activity, delayed bills, and open close exposure.

Use invoice history, inventory records, contracts, supplier patterns, usage trends, and documented assumptions.

Report accrual amounts, cost center impact, approval status, reversal timing, variance, and reconciliation status.